About me

Cardless Cash

Cardless Cash

My Role

Company

Type

Team

When

Tools

UX and prototyping

NCR

Product management request

Katie Foster

2021

Figma

Background

This feature was requested by product management and needed to seamlessly integrate into the existing NCR D3 banking app. The solution adheres strictly to all components and patterns utilized by NCR D3 at that time, ensuring a consistent user experience. Because requirements were defined upfront by PM and compliance teams, the design challenge wasn't about what to build, it was about how to make tightly constrained interactions feel effortless. Fixed withdrawal amounts, expiring access codes, and a multi-currency scope were all non-negotiable. The work was in the flow.

Personas

Both users share a common need: access to cash without a physical card, but arrive at the feature from very different contexts. The design had to serve both without privileging one.

Name

Age

Location

Occupation

Primary need

Trigger

Frustration

Samuel

38

Chicago, IL

Operations manager

Withdraw cash without needing his physical card

Left wallet at home, needs cash now

Feeling stranded by a preventable problem

Samuel is a mid-level professional in his late 30s based in Chicago. He uses cash regularly for everyday expenses: coffee, parking, the occasional farmers market, but his wallet is an afterthought. He's left it at home more than once and found himself unable to withdraw cash at a critical moment. His current workaround is either abandoning the transaction or making a second trip, both of which frustrate him. He's highly comfortable with mobile banking and expects his phone to solve problems his physical wallet can't. Security isn't top of mind for him unless something goes wrong, but when it does, it permanently changes how he feels about his bank.

Name

Age

Location

Occupation

Primary need

Trigger

Frustration

Maya

42

New York, NY

Senior consultant

Access cash abroad without carrying or exposing her physical debit card

Traveling internationally, prefers not to use her card at foreign ATMs

Banking apps that feel designed only for domestic, low-risk scenarios

Maya is a senior consultant in her early 40s who travels internationally four to six times a year for work. She's meticulous about security when abroad, she's heard enough card skimming horror stories from colleagues that she deliberately leaves her debit card in the hotel safe when exploring unfamiliar cities. But she still needs local cash. She wants a way to withdraw money at a foreign ATM without exposing her physical card, and she expects her banking app to support the currency and language of wherever she happens to be. She's a power user and reads the fine print, notices when something feels off, and will switch banks if the experience doesn't match her level of sophistication.

Requirements

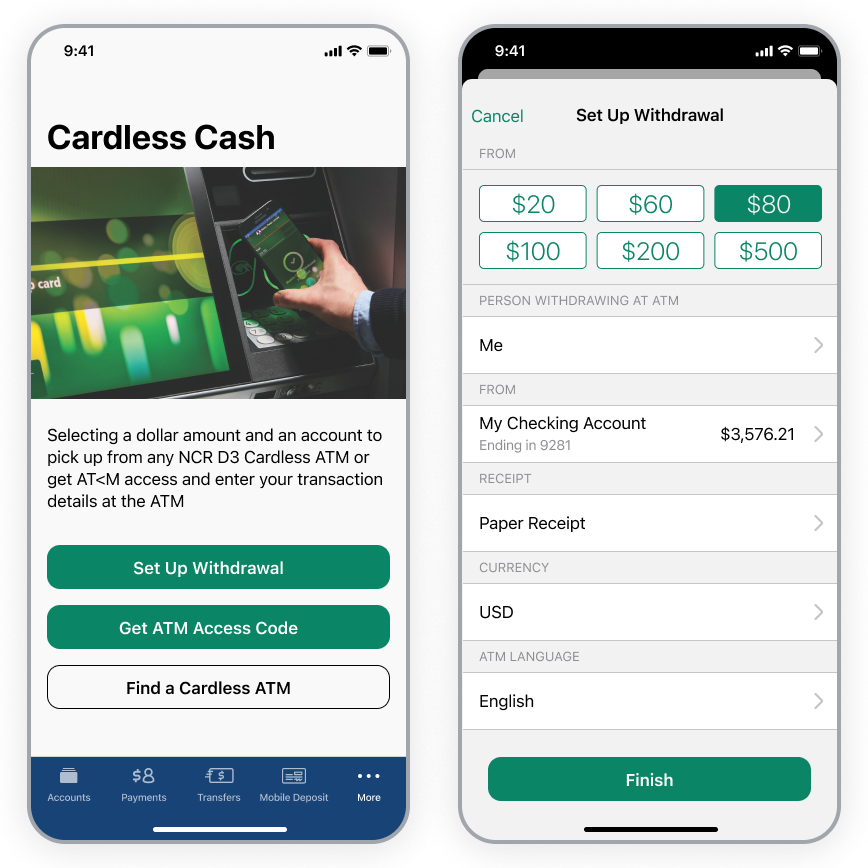

"Let users withdraw cash from an ATM without needing their physical debit card."

- Support pre-staging a withdrawal (set amount + account before arriving at the ATM)

- Limit withdrawal amounts to a fixed set ($20, $60, $80, $100, $200, $500) rather than free entry (most common withdrawal amounts)

- Generate a one-time access code that expires on a timer

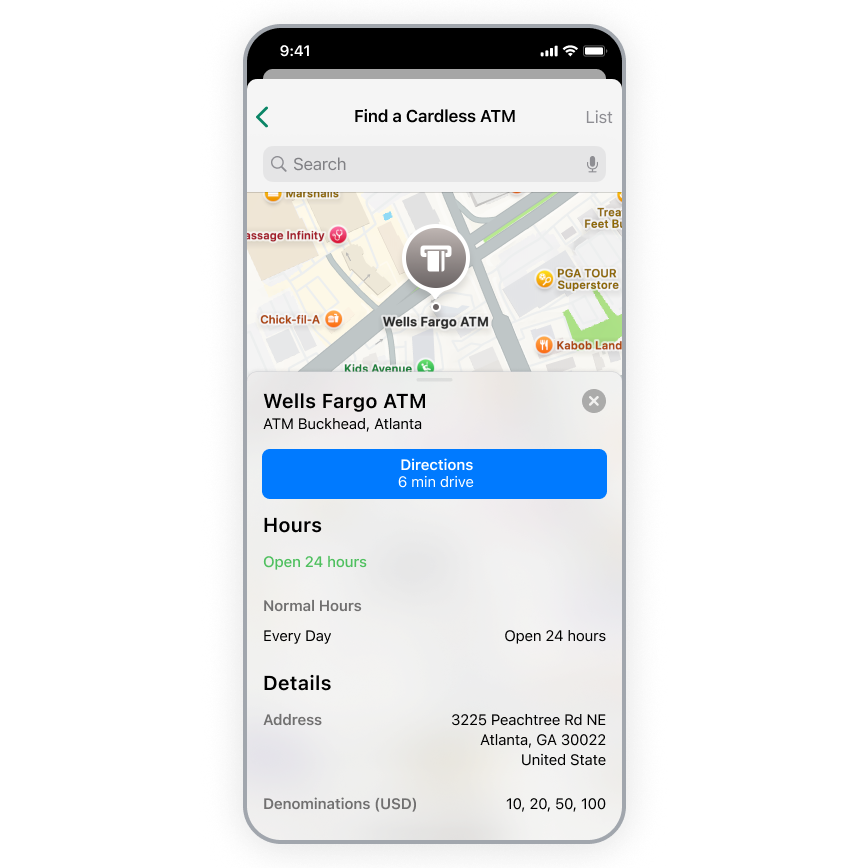

- Let users find a compatible ATM nearby

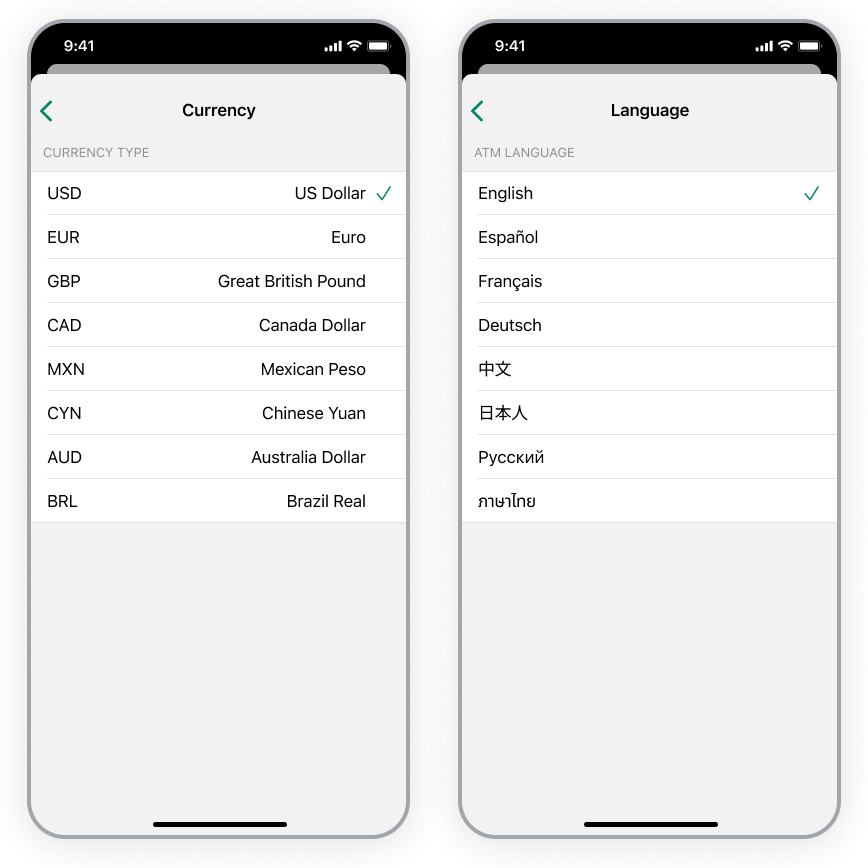

- Support multiple currencies and languages (suggesting this was scoped for international markets or a diverse domestic user base)

- Offer a receipt toggle (regulatory/accessibility requirement)

Target success criteria

This feature work did not have any defined success criteria, but these are some I would have tracked towards to.

Adoption

10%

of total mobile initated withdrawals

Funnel

90%

start vs. finishing code generation flow

Trust

50%

reuse rate

Business

< 2%

failed transaction rate

Information architecture

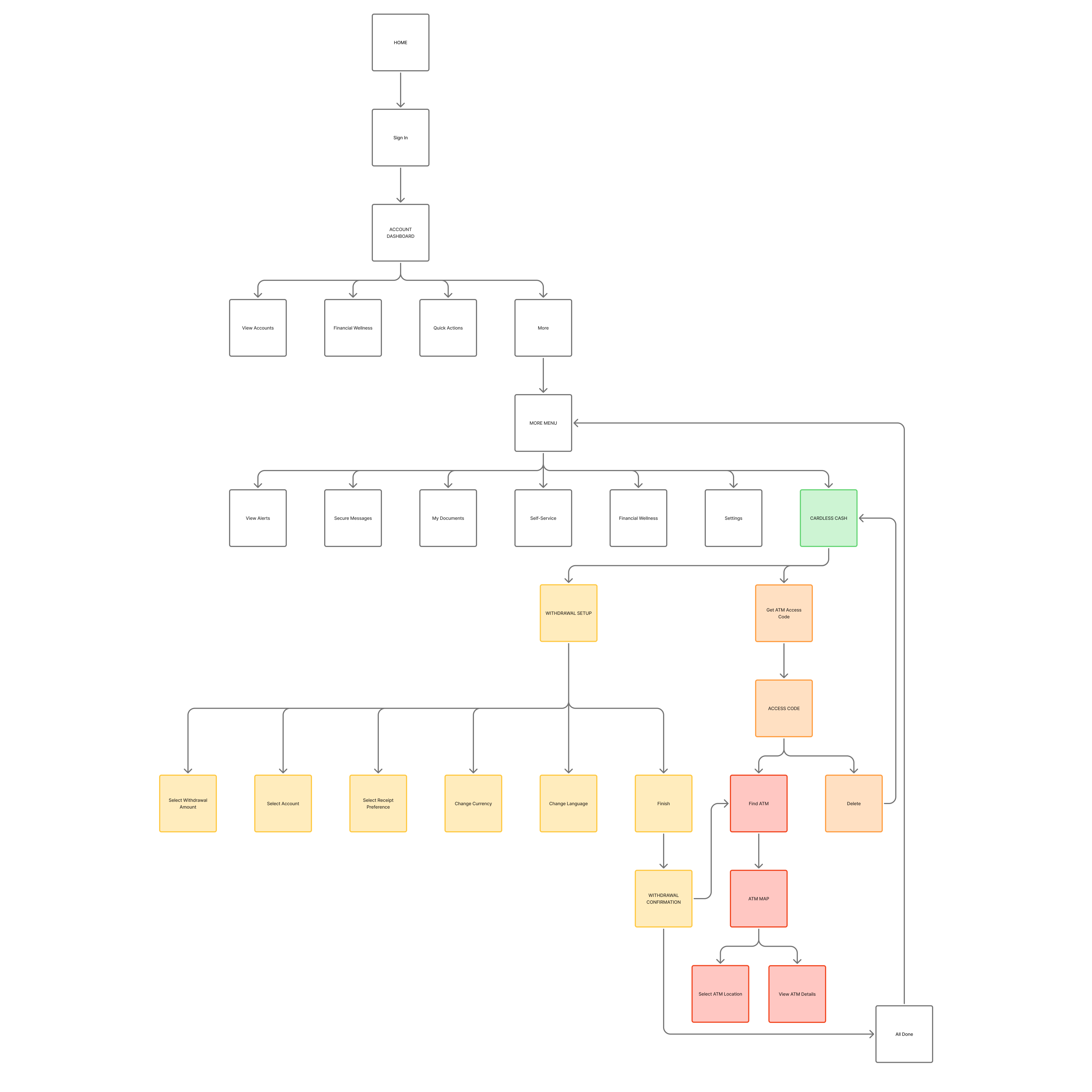

The feature had to step into the existing NCR D3 banking app. As a lower-frequency, utility-focused feature, Cardless Cash sits appropriately under the 'More' menu. Consistent with NCR D3's navigation pattern of reserving primary navigation for everyday actions and grouping occasional-use features in a secondary hub.

Requirement → Outcome

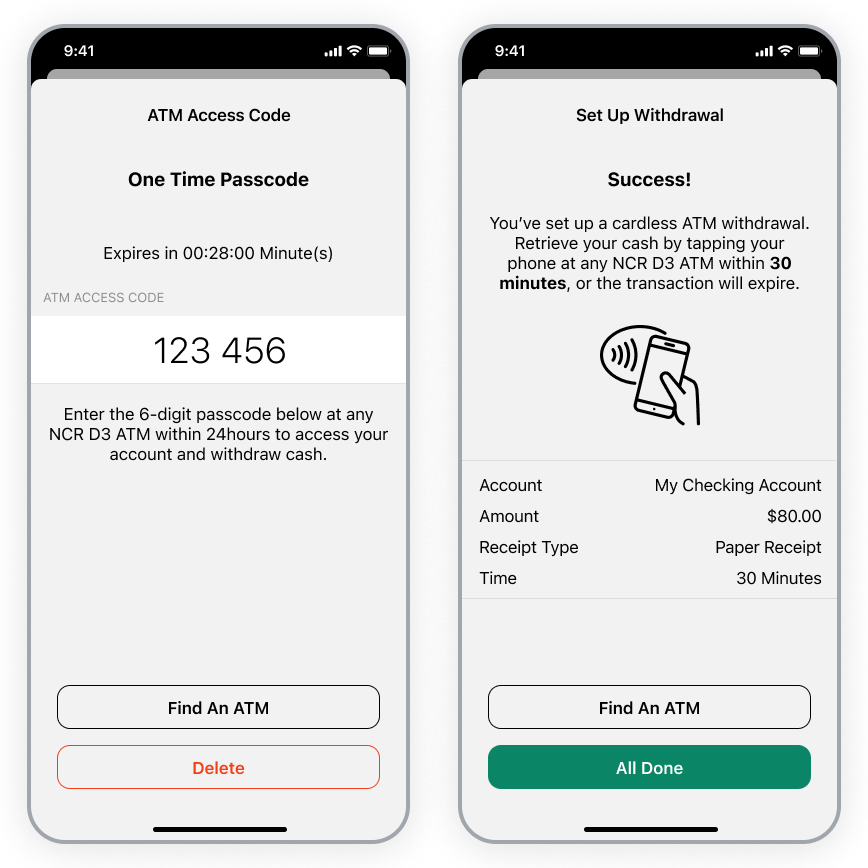

Each requirement defined by the product team maps directly to a screen or interaction in the final design. Rather than treating these as a checklist, the design work focused on making each constraint feel like a feature, particularly the fixed amounts (which reduce decision fatigue) and the timed access code (which communicates security without explaining it).

Enable pre-staged transactions

Let users withdraw cash from an ATM without needing their physical debit card.

Currency and language

Support multiple currencies and languages (suggesting this was scoped for international markets or a diverse domestic user base)

Find enabled ATMs

Let users find a compatible ATM nearby

Withdraw without card

- Generate a one-time access code that expires on a timer

- Support pre-staging a withdrawal

Reflection

This project was delivered within a defined scope with limited user research, a common reality in product work. Given more time, I would want to validate two assumptions: first, whether the 30 minute code window is actually sufficient for the average user's travel time to an ATM; observational research at ATM locations would inform this. Second, the three-path structure on the Cardless Cash landing screen assumes users arrive with a clear intent. Usability testing would reveal whether users understand the difference between 'set up a withdrawal' and 'get an access code' or whether those two paths should be collapsed into one. I'd also explore progressive disclosure for the currency and language settings, which currently surface early in a flow where most domestic users will never need them.

About me

Cardless Cash

Cardless Cash

My Role

Company

Type

Team

When

Tools

UX and prototyping

NCR

Product management request

Katie Foster

2021

Figma

Background

This feature was requested by product management and needed to seamlessly integrate into the existing NCR D3 banking app. The solution adheres strictly to all components and patterns utilized by NCR D3 at that time, ensuring a consistent user experience. Because requirements were defined upfront by PM and compliance teams, the design challenge wasn't about what to build, it was about how to make tightly constrained interactions feel effortless. Fixed withdrawal amounts, expiring access codes, and a multi-currency scope were all non-negotiable. The work was in the flow.

Personas

Both users share a common need: access to cash without a physical card, but arrive at the feature from very different contexts. The design had to serve both without privileging one.

Name

Age

Location

Occupation

Primary need

Trigger

Frustration

Samuel

38

Chicago, IL

Operations manager

Withdraw cash without needing his physical card

Left wallet at home, needs cash now

Feeling stranded by a preventable problem

Samuel is a mid-level professional in his late 30s based in Chicago. He uses cash regularly for everyday expenses: coffee, parking, the occasional farmers market, but his wallet is an afterthought. He's left it at home more than once and found himself unable to withdraw cash at a critical moment. His current workaround is either abandoning the transaction or making a second trip, both of which frustrate him. He's highly comfortable with mobile banking and expects his phone to solve problems his physical wallet can't. Security isn't top of mind for him unless something goes wrong, but when it does, it permanently changes how he feels about his bank.

Name

Age

Location

Occupation

Primary need

Trigger

Frustration

Maya

42

New York, NY

Senior consultant

Access cash abroad without carrying or exposing her physical debit card

Traveling internationally, prefers not to use her card at foreign ATMs

Banking apps that feel designed only for domestic, low-risk scenarios

Maya is a senior consultant in her early 40s who travels internationally four to six times a year for work. She's meticulous about security when abroad, she's heard enough card skimming horror stories from colleagues that she deliberately leaves her debit card in the hotel safe when exploring unfamiliar cities. But she still needs local cash. She wants a way to withdraw money at a foreign ATM without exposing her physical card, and she expects her banking app to support the currency and language of wherever she happens to be. She's a power user and reads the fine print, notices when something feels off, and will switch banks if the experience doesn't match her level of sophistication.

Requirements

"Let users withdraw cash from an ATM without needing their physical debit card."

- Support pre-staging a withdrawal (set amount + account before arriving at the ATM)

- Limit withdrawal amounts to a fixed set ($20, $60, $80, $100, $200, $500) rather than free entry (most common withdrawal amounts)

- Generate a one-time access code that expires on a timer

- Let users find a compatible ATM nearby

- Support multiple currencies and languages (suggesting this was scoped for international markets or a diverse domestic user base)

- Offer a receipt toggle (regulatory/accessibility requirement)

Target success criteria

This feature work did not have any defined success criteria, but these are some I would have tracked towards to.

Adoption

10%

of total mobile initated withdrawals

Funnel

90%

start vs. finishing code generation flow

Trust

50%

reuse rate

Business

< 2%

failed transaction rate

Information architecture

The feature had to step into the existing NCR D3 banking app. As a lower-frequency, utility-focused feature, Cardless Cash sits appropriately under the 'More' menu. Consistent with NCR D3's navigation pattern of reserving primary navigation for everyday actions and grouping occasional-use features in a secondary hub.

Requirement → Outcome

Each requirement defined by the product team maps directly to a screen or interaction in the final design. Rather than treating these as a checklist, the design work focused on making each constraint feel like a feature, particularly the fixed amounts (which reduce decision fatigue) and the timed access code (which communicates security without explaining it).

Enable pre-staged transactions

Let users withdraw cash from an ATM without needing their physical debit card.

Currency and language

Support multiple currencies and languages (suggesting this was scoped for international markets or a diverse domestic user base)

Find enabled ATMs

Let users find a compatible ATM nearby

Withdraw without card

- Generate a one-time access code that expires on a timer

- Support pre-staging a withdrawal

Reflection

This project was delivered within a defined scope with limited user research, a common reality in product work. Given more time, I would want to validate two assumptions: first, whether the 30 minute code window is actually sufficient for the average user's travel time to an ATM; observational research at ATM locations would inform this. Second, the three-path structure on the Cardless Cash landing screen assumes users arrive with a clear intent. Usability testing would reveal whether users understand the difference between 'set up a withdrawal' and 'get an access code' or whether those two paths should be collapsed into one. I'd also explore progressive disclosure for the currency and language settings, which currently surface early in a flow where most domestic users will never need them.

About me

Cardless Cash

Cardless Cash

My Role

Company

Type

Team

When

Tools

UX and prototyping

NCR

Product management request

Katie Foster

2021

Figma

Background

This feature was requested by product management and needed to seamlessly integrate into the existing NCR D3 banking app. The solution adheres strictly to all components and patterns utilized by NCR D3 at that time, ensuring a consistent user experience. Because requirements were defined upfront by PM and compliance teams, the design challenge wasn't about what to build, it was about how to make tightly constrained interactions feel effortless. Fixed withdrawal amounts, expiring access codes, and a multi-currency scope were all non-negotiable. The work was in the flow.

Personas

Both users share a common need: access to cash without a physical card, but arrive at the feature from very different contexts. The design had to serve both without privileging one.

Name

Age

Location

Occupation

Primary need

Trigger

Frustration

Samuel

38

Chicago, IL

Operations manager

Withdraw cash without needing his physical card

Left wallet at home, needs cash now

Feeling stranded by a preventable problem

Samuel is a mid-level professional in his late 30s based in Chicago. He uses cash regularly for everyday expenses: coffee, parking, the occasional farmers market, but his wallet is an afterthought. He's left it at home more than once and found himself unable to withdraw cash at a critical moment. His current workaround is either abandoning the transaction or making a second trip, both of which frustrate him. He's highly comfortable with mobile banking and expects his phone to solve problems his physical wallet can't. Security isn't top of mind for him unless something goes wrong, but when it does, it permanently changes how he feels about his bank.

Name

Age

Location

Occupation

Primary need

Trigger

Frustration

Maya

42

New York, NY

Senior consultant

Access cash abroad without carrying or exposing her physical debit card

Traveling internationally, prefers not to use her card at foreign ATMs

Banking apps that feel designed only for domestic, low-risk scenarios

Maya is a senior consultant in her early 40s who travels internationally four to six times a year for work. She's meticulous about security when abroad, she's heard enough card skimming horror stories from colleagues that she deliberately leaves her debit card in the hotel safe when exploring unfamiliar cities. But she still needs local cash. She wants a way to withdraw money at a foreign ATM without exposing her physical card, and she expects her banking app to support the currency and language of wherever she happens to be. She's a power user and reads the fine print, notices when something feels off, and will switch banks if the experience doesn't match her level of sophistication.

Requirements

"Let users withdraw cash from an ATM without needing their physical debit card."

- Support pre-staging a withdrawal (set amount + account before arriving at the ATM)

- Limit withdrawal amounts to a fixed set ($20, $60, $80, $100, $200, $500) rather than free entry (most common withdrawal amounts)

- Generate a one-time access code that expires on a timer

- Let users find a compatible ATM nearby

- Support multiple currencies and languages (suggesting this was scoped for international markets or a diverse domestic user base)

- Offer a receipt toggle (regulatory/accessibility requirement)

Target success criteria

This feature work did not have any defined success criteria, but these are some I would have tracked towards to.

Adoption

10%

of total mobile initated withdrawals

Funnel

90%

start vs. finishing code generation flow

Trust

50%

reuse rate

Business

< 2%

failed transaction rate

Information architecture

The feature had to step into the existing NCR D3 banking app. As a lower-frequency, utility-focused feature, Cardless Cash sits appropriately under the 'More' menu. Consistent with NCR D3's navigation pattern of reserving primary navigation for everyday actions and grouping occasional-use features in a secondary hub.

Requirement → Outcome

Each requirement defined by the product team maps directly to a screen or interaction in the final design. Rather than treating these as a checklist, the design work focused on making each constraint feel like a feature, particularly the fixed amounts (which reduce decision fatigue) and the timed access code (which communicates security without explaining it).

Enable pre-staged transactions

Let users withdraw cash from an ATM without needing their physical debit card.

Currency and language

Support multiple currencies and languages (suggesting this was scoped for international markets or a diverse domestic user base)

Find enabled ATMs

Let users find a compatible ATM nearby

Withdraw without card

- Generate a one-time access code that expires on a timer

- Support pre-staging a withdrawal

Reflection

This project was delivered within a defined scope with limited user research, a common reality in product work. Given more time, I would want to validate two assumptions: first, whether the 30 minute code window is actually sufficient for the average user's travel time to an ATM; observational research at ATM locations would inform this. Second, the three-path structure on the Cardless Cash landing screen assumes users arrive with a clear intent. Usability testing would reveal whether users understand the difference between 'set up a withdrawal' and 'get an access code' or whether those two paths should be collapsed into one. I'd also explore progressive disclosure for the currency and language settings, which currently surface early in a flow where most domestic users will never need them.

About me

Cardless Cash

Cardless Cash

My Role

Company

Type

Team

When

Tools

UX and prototyping

NCR

Product management request

Katie Foster

2021

Figma

Background

This feature was requested by product management and needed to seamlessly integrate into the existing NCR D3 banking app. The solution adheres strictly to all components and patterns utilized by NCR D3 at that time, ensuring a consistent user experience. Because requirements were defined upfront by PM and compliance teams, the design challenge wasn't about what to build, it was about how to make tightly constrained interactions feel effortless. Fixed withdrawal amounts, expiring access codes, and a multi-currency scope were all non-negotiable. The work was in the flow.

Personas

Both users share a common need: access to cash without a physical card, but arrive at the feature from very different contexts. The design had to serve both without privileging one.

Name

Age

Location

Occupation

Primary need

Trigger

Frustration

Samuel

38

Chicago, IL

Operations manager

Withdraw cash without needing his physical card

Left wallet at home, needs cash now

Feeling stranded by a preventable problem

Samuel is a mid-level professional in his late 30s based in Chicago. He uses cash regularly for everyday expenses: coffee, parking, the occasional farmers market, but his wallet is an afterthought. He's left it at home more than once and found himself unable to withdraw cash at a critical moment. His current workaround is either abandoning the transaction or making a second trip, both of which frustrate him. He's highly comfortable with mobile banking and expects his phone to solve problems his physical wallet can't. Security isn't top of mind for him unless something goes wrong, but when it does, it permanently changes how he feels about his bank.

Name

Age

Location

Occupation

Primary need

Trigger

Frustration

Maya

42

New York, NY

Senior consultant

Access cash abroad without carrying or exposing her physical debit card

Traveling internationally, prefers not to use her card at foreign ATMs

Banking apps that feel designed only for domestic, low-risk scenarios

Maya is a senior consultant in her early 40s who travels internationally four to six times a year for work. She's meticulous about security when abroad, she's heard enough card skimming horror stories from colleagues that she deliberately leaves her debit card in the hotel safe when exploring unfamiliar cities. But she still needs local cash. She wants a way to withdraw money at a foreign ATM without exposing her physical card, and she expects her banking app to support the currency and language of wherever she happens to be. She's a power user and reads the fine print, notices when something feels off, and will switch banks if the experience doesn't match her level of sophistication.

Requirements

"Let users withdraw cash from an ATM without needing their physical debit card."

- Support pre-staging a withdrawal (set amount + account before arriving at the ATM)

- Limit withdrawal amounts to a fixed set ($20, $60, $80, $100, $200, $500) rather than free entry (most common withdrawal amounts)

- Generate a one-time access code that expires on a timer

- Let users find a compatible ATM nearby

- Support multiple currencies and languages (suggesting this was scoped for international markets or a diverse domestic user base)

- Offer a receipt toggle (regulatory/accessibility requirement)

Target success criteria

This feature work did not have any defined success criteria, but these are some I would have tracked towards to.

Adoption

10%

of total mobile initated withdrawals

Funnel

90%

start vs. finishing code generation flow

Trust

50%

reuse rate

Business

< 2%

failed transaction rate

Information architecture

The feature had to step into the existing NCR D3 banking app. As a lower-frequency, utility-focused feature, Cardless Cash sits appropriately under the 'More' menu. Consistent with NCR D3's navigation pattern of reserving primary navigation for everyday actions and grouping occasional-use features in a secondary hub.

Requirement → Outcome

Each requirement defined by the product team maps directly to a screen or interaction in the final design. Rather than treating these as a checklist, the design work focused on making each constraint feel like a feature, particularly the fixed amounts (which reduce decision fatigue) and the timed access code (which communicates security without explaining it).

Enable pre-staged transactions

Let users withdraw cash from an ATM without needing their physical debit card.

Currency and language

Support multiple currencies and languages (suggesting this was scoped for international markets or a diverse domestic user base)

Find enabled ATMs

Let users find a compatible ATM nearby

Withdraw without card

- Generate a one-time access code that expires on a timer

- Support pre-staging a withdrawal

Reflection

This project was delivered within a defined scope with limited user research, a common reality in product work. Given more time, I would want to validate two assumptions: first, whether the 30 minute code window is actually sufficient for the average user's travel time to an ATM; observational research at ATM locations would inform this. Second, the three-path structure on the Cardless Cash landing screen assumes users arrive with a clear intent. Usability testing would reveal whether users understand the difference between 'set up a withdrawal' and 'get an access code' or whether those two paths should be collapsed into one. I'd also explore progressive disclosure for the currency and language settings, which currently surface early in a flow where most domestic users will never need them.